Alt Investments

EXCLUSIVE: Hedge Funds: Time To Exit Or Are They Still Worth The Effort?

Recent market turmoil - as in China - casts fresh light on an argument that has been around for some time: are hedge funds worthwhile?

The violent intra-day market volatility seen in the past two

weeks has caused widespread panic and has undoubtedly seen many

investors making irrational and emotionally-driven decisions.

These decisions often don’t achieve the best-possible results and

destroy investors’ wealth. It is in times like these when hedge

funds can prove their worth by protecting investors against the

full extent of the losses experienced by their long-only

counterparts. The relative flexibility of hedge fund strategies,

this article argues, also allows them to capitalise on the

opportunities brought about by these extreme market

movements.

Paul Wiseman, who is a London-based senior investment analyst

with Maitland, the

South Africa-based law firm and funds administrator, explains why

hedge funds still have a place in investment portfolios – and

even more so in the light of recent events. This article is being

published in different regions because of the global significance

of the issues at stake. And the main issue might be reframed

thus: for their fees and complexities, are hedge funds worth the

trouble, or do they still form an important potential part of the

wealth management toolkit?

Recent years have seen meagre returns relative to equities for

the average global hedge fund, while most cheap and cheerful

index trackers have produced solid gains. As a result, for those

investors who have carried allocations to hedge fund strategies

in place of more traditional asset classes, the role of hedge

funds has come into question. These concerns are driven largely

by the relative underperformance and the ongoing debate over

excessive fees in the hedge fund industry. It ignores the fact

that the inclusion of hedge funds in a particular portfolio may

well be entirely the result of a desire not to have more

traditional asset class exposure.

Performance fatigue

Indeed most criticism fails to address market exposure

differences between hedge funds and long-only passive products.

On average, hedge funds are neither fully exposed (beta of one)

nor are they fully hedged (beta of zero) to equity markets. It

should therefore come as no surprise that hedge funds tend to

underperform when markets rally strongly, and lose some money

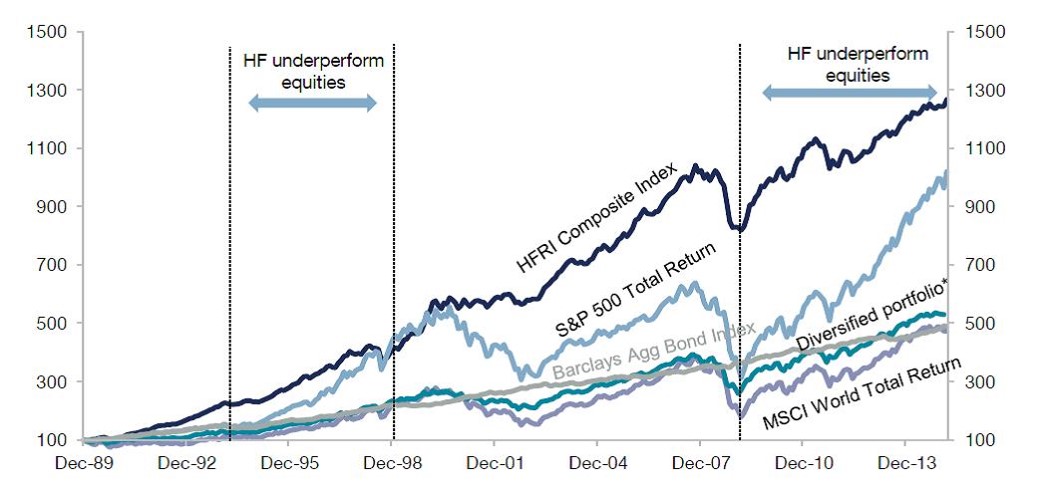

when markets sell off. Figure 1 compares hedge fund performance

(HFRI Composite Index) to that of equities, fixed income and a

generic, diversified portfolio of long-only assets over time. It

is clear that there have been extended periods of out- and

underperformance, and we are currently almost seven years into a

sustained period of underperformance. The chart reflects the

cumulative growth of a hypothetical $100 invested in each of the

asset classes listed. While hedge funds have outperformed over

the very long term, there are periods in between when other

asset classes have performed better.

Figure 1: The long-term track record of hedge funds

Diversified portfolio is 60 per cent MSCI World Index / 40

per cent Barclays Global Aggregate Bond Index

Source: Lyxor Asset Management

The decision to include hedge funds as part of a portfolio is

often influenced by the type of investor in question. Certain

investors, primarily ultra high net worth individuals, view hedge

funds as high performance strategies that should outperform more

traditional investments such as long-only equity or fixed income

funds. Hedge funds charge high fees and are managed by some of

the most talented people in the money management industry – and

so it is fair enough to quickly come to a conclusion that hedge

funds should be a pure outperformance product. But we think there

is more to it than this.

Understand what you are buying

Hedge funds can play widely varying roles within a portfolio.

They are often quite specific in nature and may often be used to

fulfil a specific role in the portfolio construction process or

to provide access to certain exposures, themes or ideas that are

otherwise not possible within the more conventional approaches

offered by long-only funds.

As with any investment decision, its success or failure is

assessed relative to the desired outcome. So what might these

desired outcomes be if it is not simply about providing

outperformance relative to long-only products?

Managing your downside risk

Whilst volatility is an imperfect measure of risk it is

nonetheless a useful metric when appraising portfolio

performance, particularly in comparing a portfolio’s downside and

upside volatility (that is, do you get more performance in up

months than what you lose in down months?). The ability of hedge

funds to short, use leverage and implement derivative structures

means that hedge funds often tend to have low correlations to

traditional long-only assets, which can be comforting during

turbulent periods for capital markets.

The combination of dampened volatility (be it downside or total)

and low correlations is an attractive proposition for an investor

considering their overall portfolio – adding such positions to a

traditional portfolio will reduce the total risk of the portfolio

but could increase or maintain long-term returns.

The primary form of defence available to asset allocators faced

with expensive assets or markets is to underweight these assets

relative to a designated benchmark. This doesn’t allow for the

opportunity to directly benefit from a decline in the price of

these assets, nor does it allow for the improvement in a

portfolio’s construction by adding uncorrelated positions. This

is where hedge funds can be useful.

Consider the macro environment

While the last few years have been characterised by low

volatility (in equities, fixed income and currencies) and low

dispersion (that is most companies have benefitted from the wave

of liquidity, irrespective of how well they have performed

operationally) this benign environment cannot persist forever.

The withdrawal of quantitative easing by the US Fed and the

re-assertion of fundamental factors on asset prices should drive

US markets back towards a state of relative normality. This

process of adjustment is likely to create opportunities for those

who are more flexible than their long-only

counterparts.

Other central banks, most notably the European Central Bank and

Bank of Japan, continue to ease monetary policy. This global

divergence in monetary policy is a departure from prior years,

where the central banks of the developed world were following

expansionary policies, which creates opportunities particularly

in the currency and fixed income markets. The opportunity set for

relative value strategies looks a lot more attractive when assets

are not all moving in the same direction.

Aside from the technical and macro perspectives, further

opportunities exist due to activity in the corporate environment

for event driven or merger arbitrage style managers. M&A

activity has remained robust as financing remains cheap,

corporate balance sheets are in a healthy condition and

acquisitions are often accretive to earnings. This creates a

fertile environment for further corporate activity.

Fees

For some, it is all about the fees, and nowhere is this debate

more lively than with regard to hedge funds. We think the answer

is simple – be very sure you are getting what you pay for. The

relative performance versus volatility argument is even more

relevant when you consider the fees you will be paying and what

type of performance you are paying for. This is a substantive

issue in its own right which merits further debate but the short

answer is that investors should be most concerned with

performance net of fees.

It isn’t all about the upside

While on paper the returns generated by hedge funds over the last

few years have lagged long-only strategies, it is important to

assess these results in the context of the specific objectives

from a total portfolio perspective. There are certainly a large

number of hedge funds that have simply performed poorly, but

don’t ignore the others that have done what they said they would.

Yes, hedge funds are more expensive investment vehicles but when

skilfully selected and added to an existing portfolio, the

long-term benefits can more than make up for the added cost.