Strategy

How Can Wealth Managers Impress “Early Adopters”?

![]()

The author of this article contends that to impress Early Adopters, wealth managers have a range of options, such as quick "wins" such as improving timeliness of data; others are more complex like advancing customization and access to specialists.

Here is a sponsored article from FactSet on an important theme within the global wealth management industry.

By Greg King, CFA

A growing number of tech savvy investors, dubbed Early Adopters

(1), are using online tools and insight to complete their

end-to-end investment management activities virtually.

A common misconception about Early Adopters is that they tend to

be digital natives or “difficult-to-please” Millennials

(under-35s). However, since our 2018 study, Winning Clients in

the Era of Hybrid Advice, the average age of an Early Adopter has

increased from 37 to 45. Although they are comfortable with

conducting approximately two thirds of their wealth management

activities online, 78 per cent say they do so while navigating a

range of digital pain points.

Technology offers investors a degree of control and transparency,

particularly in a volatile environment, enabling clients to make

more informed decisions. The steep post-pandemic rate of

technology adoption, however, has revealed a growing digital

divide between what Early Adopters need and what wealth

management firms are able to deliver. To continue to offer a

superior digital experience to its clients, wealth managers must

urgently review and reconcile gaps in their offerings.

Advent of a digital investor

Our latest study, in collaboration with Aon, finds that Early

Adopters tend to be more “sophisticated” investors who, in

constructing portfolios, weigh up a broad range of investment

considerations.

Since the start of the pandemic, the majority of Early Adopters

have altered their investment approach to adjust to the volatile

economic environment. For example, 46 per cent of Early Adopters

are adopting a longer-term investment horizon and over half have

shifted the focus of their portfolio to growth (52 per cent vs 10

per cent of Digital Phobics).

As a result, the composition of their portfolio is also changing.

Although liquid assets remain the dominant preference for

portfolio construction, there is a tendency among Early Adopters

to prefer illiquid assets (30 per cent vs 4 per cent for Digital

Phobics) due to an extended investment horizon.

Technology offers Early Adopters greater access to information

and therefore may be the reason why a greater proportion of high

net worth individuals say they feel very confident about their

financial futures (44 per cent vs 30 per cent). It may also

explain why they are more likely to say they have adventurous

attitudes to growth of capital strategies than their less

digitally savvy counterparts.

Due to Early Adopters’ unique perspectives, their outlook differs

from other investors. For example, they are much more likely to

see international stimulus (51 per cent vs. 33 per cent) and

changes in political leadership (40 per cent vs. 17 per cent) as

opportunities rather than threats to wealth creation. They are

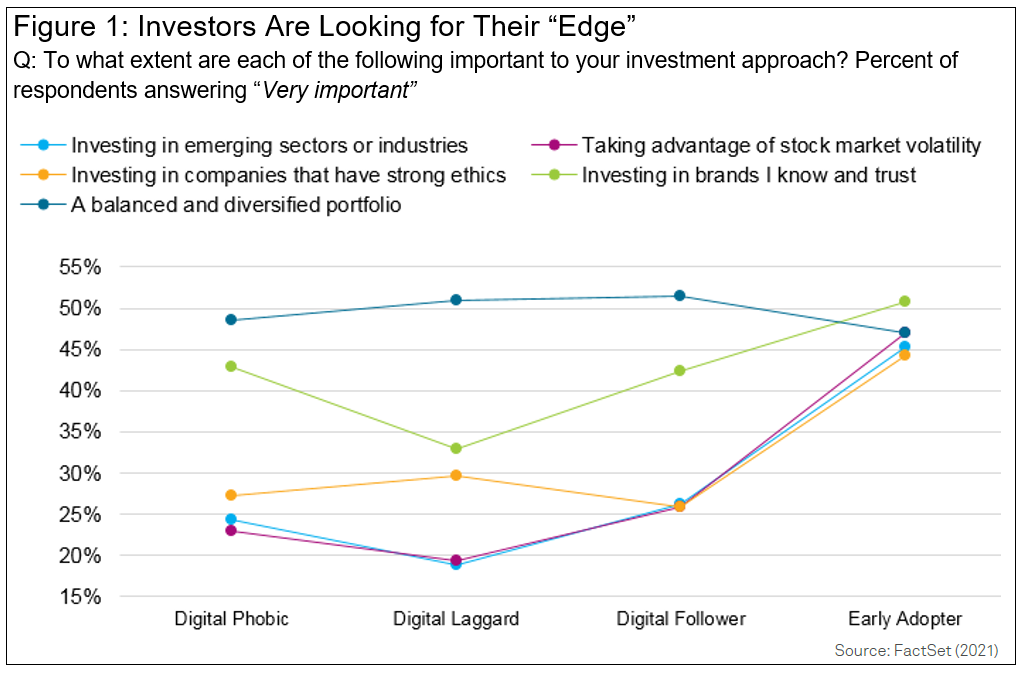

also approximately twice as likely as Digital Phobics to say it

is very important to continue investing in emerging industries

and companies that have strong ethics, while simultaneously

taking advantage of any market volatility [Figure 1].

On the other hand, low or negative interest rates are perceived

as a risk, which is perhaps why over two in five Early Adopters

say they are avoiding companies with high levels of corporate

debt (46 per cent vs 44 per cent).

Growing pains

Reliable technology is critical to Early Adopters - if they are

to continue making the most of opportunities in a rapidly

changing investment landscape.

However, they are least likely to be impressed by the digital

experience from their wealth providers, with data showing that

just 22 per cent say there are no pain points to managing their

wealth online. Indeed, only 34 per cent of Early Adopters give

their wealth manager’s digital capabilities top scores.

Some issues are easier to solve than others. One of the common

challenges is that insights delivered by their wealth managers

are not sufficiently tailored to their interests. Another is that

investment information is not timely, easy to understand or

analyze.

For example, frequently cited pain points by Early Adopters

include challenges around understanding portfolio performance (20

per cent vs 7 per cent for Digital Phobics), knowing what are the

next steps for their portfolio (22 per cent vs 4 per cent),

difficulties with reaching their advisor (17 per cent vs 4 per

cent), and the inability to see real-time data (19 per cent vs 7

per cent) [Figure 2]

It will therefore be up to each wealth manager to decide how best

to prioritize investment in improving access to real-time

insight, portal functionality, and the overall user

experience.

Figure 2:

Digital Investor Profiles for a Post-Pandemic World

(Click on the link to view.)

The new dawn

Today, clients’ expectations around the digital experience are

vastly different from only a few years ago - and continue to

advance at an incredible speed.

Because Early Adopters are the first to trial new technology and

are, to an extent, self-servicing (as they intend to conduct the

majority of their interactions digitally in future) - it’s

important for wealth managers to meet their discerning standards

and uphold their trust.

A range of innovation opportunities therefore exist to wealth

managers wanting to impress their Early Adopter clients. For

example, when thinking about missing elements in their wealth

relationship, they are six times more likely to value ease of

customization (36 per cent vs 6 per cent), and nine times more

likely to seek interactive insights (36 per cent vs 4 per cent)

and access to specialists (34 per cent vs 4 per cent), than other

clients.

A key benefit of completing more wealth management activities

online also includes clearer visibility of the products and

countries in which they are invested (26 per cent vs 14 [er

cent). Such tools are an important value add for investors, as

they provide much needed regional oversight and enable Early

Adopters to closely monitor the changing landscape.

These sets of priorities differ to other segments, who are less

digitally and financially confident, and more defensive in their

investment approach. Wealth managers should therefore seek to

address these gaps.

Conclusion

Today, most wealth managers have digital propositions that help

clients better engage with their wealth. However, the digital

divide precipitated by the pandemic between firms that have

embarked on a journey of digital transformation and those who

have been slow off the mark is growing - and is a particular

issue for Early Adopters.

While Early Adopters are open to using technology to manage their

wealth, they are unlikely to continue if their digital experience

remains riddled with issues.

To impress Early Adopters, wealth managers have a range of

options open to them. Some are quick wins like improving

timeliness of data; others are more complex like advancing

customization and access to specialists. Both are worth the

investment as innovative tools make firms more attractive not

only to Early Adopters, but also to other client segments.

Footnote

1, Early Adopters self-identify as being the first to trial and

use new technology in wealth management.

{kind=link}