WM Market Reports

UK Wealth Sector's 2022 Revenues Confounded Gloom, Cost Pressures A Concern – Compeer

This report – all 53 data-rich pages of it – explains the different revenue, margin, cost and performance characteristics of the UK's various types of wealth management industry players. It notes how private banks, for example, were clear winners in terms of interest margin rises as interest rates were put up.

The UK wealth management industry was affected to differing

degrees by market falls and the impact of higher interest rates

to curb inflation, but what is remarkable is how resilient the

sector has proven to be, according to a report from Compeer.

Falls in assets dented investment management fees, and lower

trade volumes after markets settled post-Covid meant that

commissions and brokerage fees were affected.

But what is striking is that total revenues increased by 6.1 per

cent year-on-year to an all-time high of £8.98 billion ($11.23

billion), the research organisation said in UK Wealth

Management Industry Report 2023.

There are causes for concern, however, such as cost

pressures.

Compeer said there is still a “huge variance” in profitability

across the sector with a large proportion still loss making or

earning very little margin.

The study is based on a Compeer “universe” of 162 firms (down

from 169 in 2020). Within that total, there are 13 execution-only

stockbrokers; 33 full-service wealth managers; 102 investment

managers, and 24 private banks.

This is an industry going through consolidation. During 2022 and

into 2023, for example, several corporate “marriages” and

takeovers took place, such as RBC’s purchase of Brewin Dolphin,

Canaccord Genuity’s acquisition of Punter Southall Wealth;

Investec Wealth & Investment’s purchase of Murray Asset

Management, and the Rathbones/Investec merger.

Moving in

Inflows have been a cause of comfort, it said.

“With over £100 billion of private client assets lost as a result

of the sharp fall in market values, it is not a surprise that

overall assets managed and administered by the sector fell to

£1.27 trillion, a year-on-year reduction of 7.5 per cent,” it

said. “However, asset inflows remain very high, both from within

and from external sources. We also continue to see new entrants

join the industry and UK wealth firms remain an attractive

investment opportunity for private equity firms as they back the

consolidators from within. Also, as we move into 2023, we have

started to see the recovery and so assets have once again moved

above £1.3 trillion in the first quarter, showing another speedy

bounce back and why firms still have optimistic growth strategies

in the coming years.”

Interest

The 53-page report noted that a “saviour” for firms last year was

a significant rise in net interest income caused by higher

interest rates – a factor that is particularly important for

private banks whose margins had been squeezed for years by

ultra-low rates after the 2008 crash.

“With the rise in interest rates, wealth management and

execution-only firms saw interest margin double, treble or even

quadruple year-on-year and this has more than compensated for the

fall in other revenue streams,” it said.

“For full-service wealth managers and investment managers, with

net interest income representing only a small percentage of total

revenue, although they have benefitted it has had less of an

overall impact,” the report said.

“That leaves the execution-only stockbrokers for whom the change

has been most radical. Net interest income has gone from 4 per

cent of revenue in 2021 to more than a quarter of all

execution-only revenue in 2022! This therefore surpassed

commissions in the revenue stream table. Clients too are

benefiting as these firms are now able to offer interest back on

balances held in cash, something they have been unable to do in

the previous three years,” it said.

Costs problem

But as Compeer noted, while revenue results surprised on the

upside, the control of costs is a problem.

Total costs, the report said, increased by 6.1 per cent (the same

percentage growth as total revenue). This was primarily driven by

further investment in technology (total IT costs surpassed £1

billion for the first time in 2022) as firms continue to embrace

the digital revolution and upgrade systems to achieve efficiency

gains.

The report noted that hiring staff – adding 42,000 people – added

to costs, and rising wage bills turned the screws further.

“Therefore, pre-tax profit margins remain under pressure and many

in the industry failed to deliver scalable results during the

year,” it continued.

“With the exception of private banks, where the absolute impact

from net interest income rises was enough to raise the

profitability of these firms, other firm types reported

reductions in pre-tax profit margins,” it said.

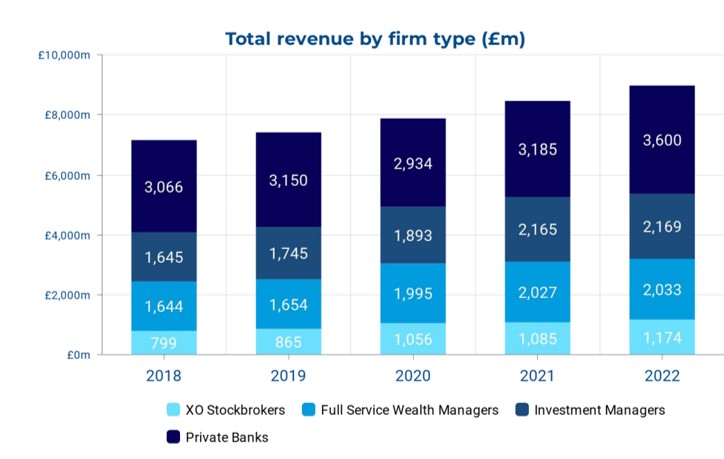

Revenue by type

The report broke down revenues by the type of firm and how this

changed:

Source: Compeer

This news service will continue to draw on extracts from this

comprehensive report, as part of our coverage as exclusive

media partner with Compeer. Here is its website.