Asset Management

UK Squeeze On Retail Savings Highlights Money Market Funds' Appeal – Aviva Investors

The investment group is one of the players in the field of money market funds – a large market in the US and certain other nations, but less so in the UK. Given recent tax changes and the likely interest rate path, that's an oversight, so Aviva Investors argues.

When the UK finance minister, aka Chancellor of the Exchequer,

Rachel Reeves, squeezed the tax allowances for retail cash

savings accounts last year, it forced some wealth managers to

rethink how cash is put to work.

Such a move puts money market funds – still a relatively nascent

sector in the UK compared with places such as the US – in a

potentially favourable spotlight.

Alastair Sewell (pictured below), senior investment strategist at

Aviva Investors, said Reeves’ tightening of allowances on cash

ISAs may be a teachable moment. Reeves cut the annual cash ISA

allowance from £20,000 ($26,705) to £12,000, starting from April

2027.

Alastair Sewell

“In the UK, money market funds remain underutilised. Bank

deposits often pay rates below the Bank of England base rate and

cash benchmarks,” Sewell told WealthBriefing in a recent

call. “This environment could trigger a broader re-think of money

market funds in the UK.”

According to one definition from BlackRock, a money market fund

is a type of mutual fund, typically holding cash, government

securities or repurchase agreements collateralised by government

securities. Some MMFs can hold government securities, but also

those issued by banks, corporations and non-government bodies. In

the US, another form of fund are those linked to municipalities

that hold municipal securities; earnings are typically exempt

from federal tax. Standard MMFs have a minimum investment horizon

of three months and offer the opportunity of yield uplift.

Aviva sees wealth managers as an important audience for its

funds.

“We continue to engage closely with wealth managers, private

banks and other clients through our regular market insights and

educational materials,” he said.

The UK will have some way to go to get even near the US money

market sphere – the latter hit a total of $8.9 trillion in

December 2025, a record (source: Crane Data). In the UK, such

funds hold about £50 billion. US money market funds have held

stable as a share of overall US mutual fund assets for years –

accounting for 17 per cent of total mutual fund assets, versus

only 3 per cent in the UK.

One reason why the UK has traditionally not had a large MMF

sector is because UK government bonds (gilts) are free of tax, so

they tend to be a tax-efficient alternative for money market

funds.

But change may be coming.

“Money market assets should remain fairly stable through rate

cutting,” Sewell said.

One cause for a positive approach, Sewell said, is that it is

unlikely that the UK will return to the very low interest rates

that took hold after the 2008 financial crash.

The approach

Money market funds typically provide yields materially above the

average bank deposit rates. They target a yield in line with

short-term reference rates such as SONIA (Sterling Overnight

Index Average) – the replacement for the old LIBOR interbank

measure.

“A cash allocation is an important element of most investment

portfolios. While it can be tempting to reduce that allocation in

times of falling rates, it is also important to think about

potential liquidity needs and how they can be met,” Sewell

said.

Generational shift?

One driver and hope for more growth is among younger investors; they have fewer preconceived ideas about what MMFs are and can do, Sewell said. “We might see a broad generational shift in attitudes towards wealth and investing.”

Some concerns

The UK’s Financial Conduct Authority has been reviewing how money

market funds operate, mindful of potential worries about

liquidity strains.

In December 2023, the FCA wrote in an updated consultation

document: “In March 2020, financial markets reacted sharply to

the pandemic and the public health measures introduced to contain

its spread. This shock led to an extreme and sudden ‘dash for

cash’. MMFs came under severe strain as investors withdrew money

from MMFs to meet their often rising needs for cash, and out of

fear of not being able to get their money back from their MMFs

later. This in turn increased the pressure on MMFs, increasing

the risk they would be unable to meet investors’ demands for

their money back. If multiple MMFs used by UK investors had

‘suspended’ there could have been a significant threat to wider

UK financial stability.”

Sewell noted that US dollar-denominated MMFs suffered more stress

during that episode than was the case with other currencies.

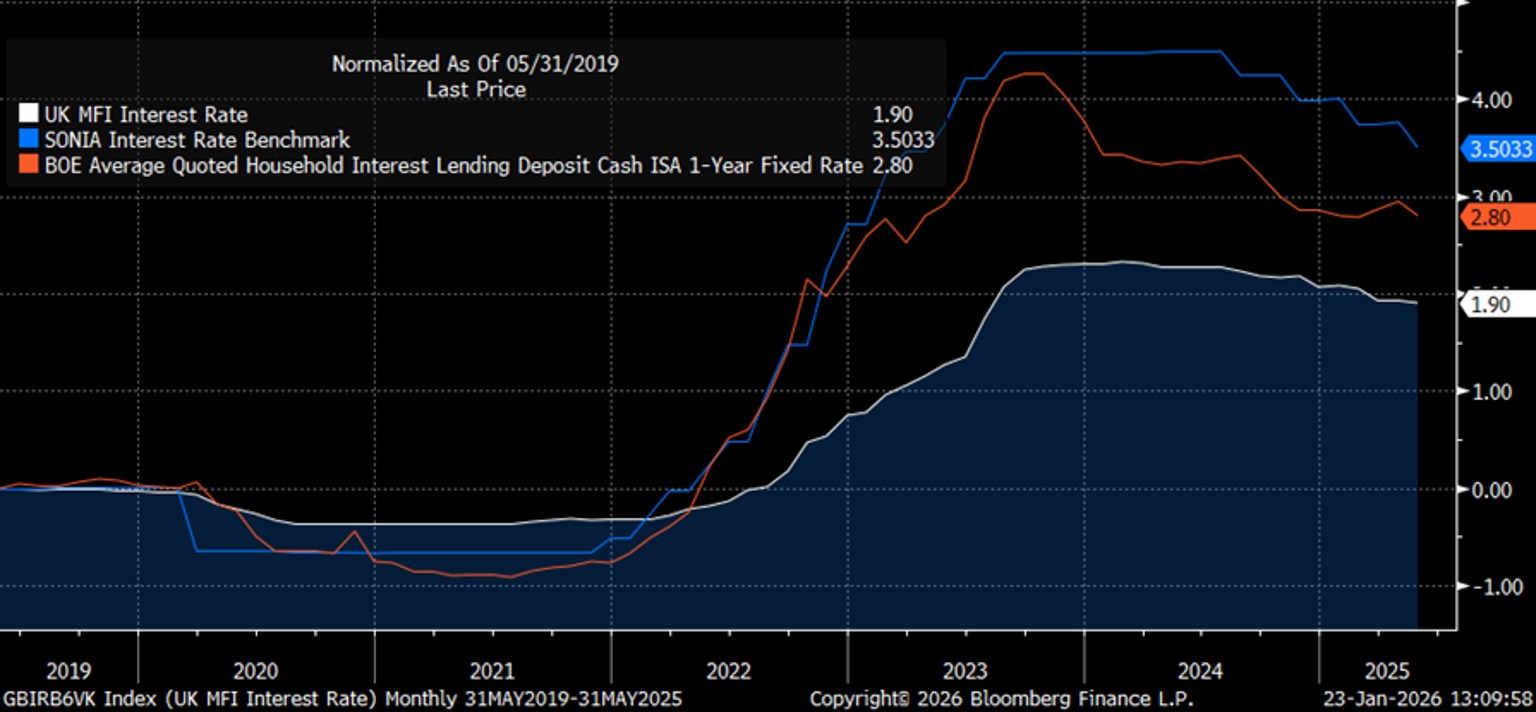

He added that the Aviva Investors Sterling Liquidity Fund yielded

4.00 per cent gross as of 22 January 2026 vs SONIA at 3.73 per

cent. According to a chart (see below), the average rate of

interest paid on UK household deposits and the average 1-year

fixed cash ISA rate are both lower than SONIA over multiple

time periods. A fixed cash ISA will not usually allow

withdrawals until scheduled times.

Source: Aviva Investors

(See this interview with Sewell, from two years ago, in which the impact of bank failures and associated volatility had put MMFs in the frame.)