Alt Investments

The "Direct Co-Investment" Route To Superior Private Market Returns – Morgan Stanley Study

There has been a large shift over the past two decades from listed public companies to privately held ones. A typical way to access this opportunity is via private equity funds. The route of "direct co-investment" deserves more attention, says Morgan Stanley.

Direct co-investment offers a way to tap into the world of

private markets without incurring some of the costs of using a

“co-mingled” fund. And, if handled correctly, investors can still

spread risks in a way that they could not achieve by doing

everything themselves, argues Morgan

Stanley Wealth Management in a recent paper.

“Today, private markets are responsible for a substantially

higher portion of innovation and value creation than in prior

years, which makes them very attractive for investors pursuing

alpha. As private market portfolios mature and return enhancement

continues to be a primary investment objective, investors may

seek to augment their exposure by accessing direct co-investments

in targeted sectors and strategies alongside favored fund

managers at more attractive fees,” the US bank said in the

report. The paper is entitled A Tug Of War: Public Versus

Private.

“Since individual direct co-investments may be deemed high risk,

investors are well advised to deploy a portfolio approach

tailored to their own needs. In this manner, investors will be

better equipped to balance the potential for upside return

against sizable downside risk while seeking to benefit from

significant potential diversification flexibility,” it said.

However, azfter fund vehicles have dominated private equity and

venture capital, the focus is switching toward direct

investing, Morgan Stanley said. For most investors, this means

that they can cut fees paid to fund managers, reduce the risk of

putting money into a “blind pool” and carry out their own due

diligence on investments. This also moves away from the

“co-mingled” funds model that has been the norm in recent years.

According to one online definition, direct co-investing is "when

an investor invests alongside a sponsor in a direct investment

and the investment is not part of a greater GP-LP blind pool fund

relationship with the sponsor."

Morgan Stanley said co-investments benefit from a variety of

forces: Private equity fund managers that want to make bigger

deals are constrained by portfolio construction guidelines that

cap the amount of equity per deal. Managers may have discretion

to allocate a portion of excess capacity to other prospective

limited partners. High net worth investors are still a relatively

untapped market for private equity funds.

Investors can gain exposure to direct co-investments either

through a co-investment fund, which are typically diversified

portfolios of co-investments within a 10-year fund structure, or

investment in individual co-investment deals. As a rule,

individual direct co-investments are structured as or through

special purpose vehicles (SPVs), with the SPV investing alongside

a lead sponsor’s fund vehicle, Morgan Stanley said.

Secular shift

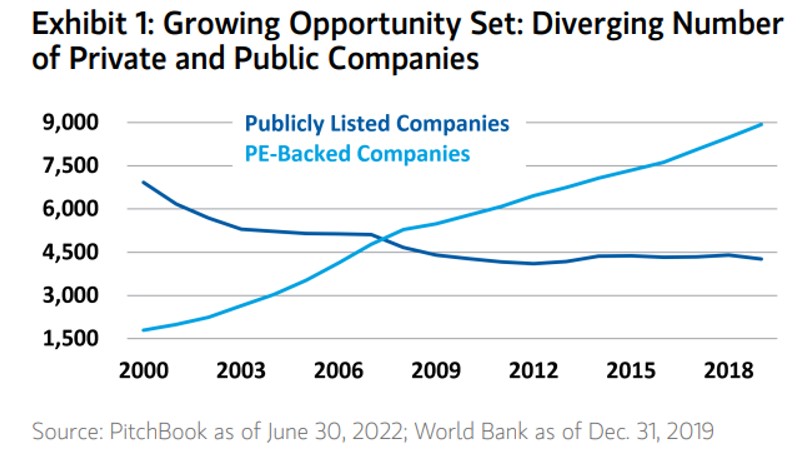

There is a secular shift in favor of private markets as firms

take longer to float on stock markets or even decline the listed

route at all. In its nine-page paper, Morgan Stanley noted that

between 2000 and 2019, the number of publicly traded US companies

collapsed by almost 40 per cent to 4,200. Conversely, the number

of private US companies backed by private equity firms surged by

almost 500 per cent, from 1,800 to 8,900.

Also, there are fewer than 3,000 public companies with annual

revenue greater than $100 million, while there are more than

14,000 private businesses with comparable revenue

levels.

There are various reasons for the shift. It is getting easier for

private equity and venture capital to attract funds. And it

continues: PricewaterhouseCoopers predicts that private markets’

AuM will rise to almost $15 trillion by 2025, versus $4.9

trillion in 2021. Another driver is the Sarbanes-Oxley Act,

introduced in the early Noughties after the Enron accounting

scandal that significantly added to regulatory burdens on listed

firms. A third headwind for public firms is the chore of handling

quarterly results and having to deal with skittish investors.