Wealth Strategies

Changing Asset Allocation Frontiers - An Overview

We take a dive into different approaches to how asset allocation should be handled, examine various views - including contrarian ones - and consider how attitudes about diversification have changed over time.

It is sometimes stated that asset allocation is the overwhelming

driver of variation in investment returns. Everything else, such

as selecting individual stocks and trying – often unsuccessfully

– to time a market, pales into insignificance.

Back in 1986, a study from Gary Brinson, Randolph Hood, and

Gilbert Beebower, - “Determinants of Portfolio Performance”

(Financial Analysts Journal, July–August 1986) stated

that almost 90 per cent of portfolio return variation is driven

by asset allocation.

The devil is in the details, however – and given the tens of

trillions of dollars/equivalents being invested today – that

leaves plenty of room for other ideas. Active management, even

with the caveats about markets being “mean-reverting” and the

challenges of sustaining outperformance, can drive considerable

performance dispersion. It is easy to make the case for “passive”

investing (that adjective can be misleading, since any decision

on how to invest is an “act”) when markets are steadily rising,

but not quite so much when markets are treading water or showing

heightened volatility.

Asset allocation is very much on people's minds. In this

final quarter of the year, thoughts can often turn towards how

wealth managers and private banks deploy clients’ money, and we

have carried a raft of commentaries about the pros and cons of

investing

in the US, the impact of a devaluing dollar;

shifts to emerging markets; the case for

Japan, or

India, and

Europe. There’s also a fair amount

of rumination about whether the old “60/40” equity/bond

balanced portfolio makes much sense when – as has happened in

recent years – stocks and bonds move in lockstep. And nowadays we

have the rise of private market investing and moves even in the

mass-affluent/retail space to

hold private market assets. Joe Public, meet the Yale

Model.

Another important topic that has caught more attention

recently is

“concentration risk”. When the “Magnificent Seven” US Big

Techs account for as much as 34 per cent of the market cap of the

S&P 500, as was the case in August, it heightens the danger

that a reversal could hit those who think they’re diversified in

holding a whole index. This leads also to concerns about whether

investors’ advisors fully grasp what sort of indices they are

exposed to, and how the reconstitution of indices can also

lead to people to miss out on rises in values of certain

firms. (See

an article here.)

The asset allocation stance taken by a high net worth or

ultra-HNW individual and family is clearly linked to risk

tolerance and their goals. That tolerance might depend on whether

the investors are still beneficial owners of an operating

business that generates cash or rely on a pool of liquid assets

after a firm has been sold. Asset allocation can also be

fine-tuned for individual family members - what’s good for

Mum and Dad if they are retired is not so appropriate for their

adult children.

It is not just asset allocation that is important in thinking

about where returns come from, but

asset “location” is significant too. Remember, it is the

after-tax returns that count. Fears that taxes such as capital

gains could rise have, along with other forces, put the location

of investments into the limelight to an extent that appears to be

relatively new by the standards of recent years. For instance,

getting details right – such as understanding whether a fund’s

share class has a particular status, incurring either capital

gains or income tax, can be crucial.

Laura Cooper, global investment strategist at Nuveen, reflected on the

“location” point.

“Asset location considerations remain central to our planning.

For example, we evaluate the relative advantages of holding

certain real assets or private infrastructure through specific

structures to optimise tax and regulatory treatment. Global

diversification is balanced with careful consideration of local

rules, and when recommending alternative or private strategies,

we ensure structures are suitable for the client’s domicile and

tax profile. Overall, we aim for alignment between asset

allocation and holding vehicles to enhance net returns,” Cooper

said.

Re-thinking 60/40

Among the reasons asset allocation ideas are changing is that

older assumptions have been severely tested. For example, a

traditional reliance on mixing equities and bonds to deliver the

goods no longer works, according to a recent White Paper from

Remi Olu-Pitan, head of multi-asset growth and income at Schroders.

“Creating resilience within portfolios requires a new approach

and a new asset mix,” Olu-Pitan said.

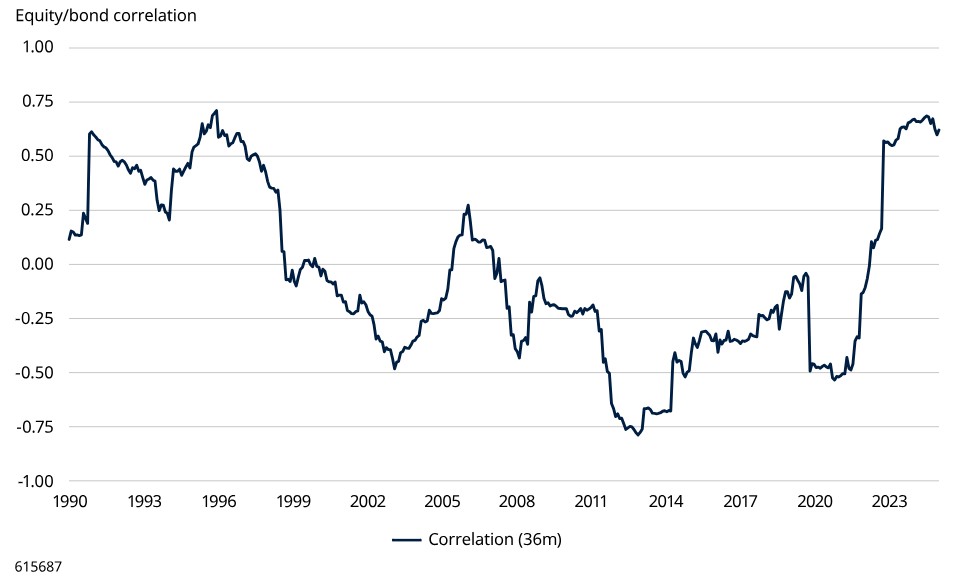

“Since 2022, global bond markets have been much more volatile and that has made bonds a less dependable source of returns,” he said. “The correlation between bond and equity returns rose significantly in the aftermath of the Covid-19 pandemic from a combination of factors that adversely affected both markets, including a spike in inflation driven by supply-chain challenges, soaring interest rates, a surge in commodity prices and geopolitical turmoil. The correlation has remained at elevated levels. As a result of all this, the 60/40 portfolio experienced severely negative returns, as exemplified by a US-focused portfolio. With its exposure to the S&P 500 Index and US Treasury bonds, the 60/40 portfolio was down nearly 18 per cent in 2023, posting its worst year since 1937,” he said.

Olu-Pitan illustrated the high correlations between bonds and stocks in the following chart:

Source: Robert Shiller, Schroders, LSEG Datastream.

Equity returns are represented by the returns of the S&P 500

Index; bonds, by the 10-year US Treasury. As at 11 July

2025.

Fresh thinking

Olu-Pitan said that bonds “still have a vital portfolio role, but

their purpose has altered”.

Bonds cannot any longer be used for downside protection during

volatile equity markets and should instead be mainly seen as an

income-generating asset, alongside other income sources. Active

portfolio management has got more important to reduce performance

dispersion; there is also a need to consider alternative

investments, such as commodities, hedge funds, private equity and

private debt, because performance drivers are so different, he

said.

Some of this loss of faith in the 60/40 model may partly explain

why, for some investors, gold has been rising this year. A

classic “safe haven” asset, it can add “ballast” to a portfolio.

The World Gold Council, the industry group that generates data on

gold markets and wider sector, is understandably positive on the

yellow metal. “The negative correlation between returns from

stocks and from bonds – once the cornerstone of a balanced

portfolio is in a state of flux due to the volatile inflation

backdrop. In terms of the implications for diversifying investor

portfolios, it remains unclear where the equity-bond correlation

will settle. But recent changes in the macroeconomic landscape

call for a cautious approach. For those investors that don’t hold

gold, this might prompt them to broaden their sources of

diversification. For those investors that already hold gold, it

might mean increasing their allocation.”

A controlled approach

In all the debates about what models work best, the time-frame

remains a crucial part of the puzzle. For a young adult, asset

allocation will be a different conversation than for someone in

late middle age counting down the years for retirement. And more

broadly still, there's a need to be composed and avoid churning

portfolios.

Chris Miles, head of UK and Ireland client group at Capital

Group, said a medium-term perspective is important to avoid being

pulled around by immediate headlines.

“The most effective approach is one anchored in long-term

thinking and deep, fundamental research. Rather than attempting

to time the market or position for binary outcomes, our process

focuses on building resilient portfolios through global

diversification and flexibility,” Miles said. “We deliberately

avoid making concentrated bets on specific scenarios, recognising

the vast array of unknowns across the global economy. Instead, we

seek to identify businesses with enduring competitive advantages,

quality leadership, robust balance sheets, and sustainable growth

potential - across regions and sectors.”

When this publication spoke to several investment houses, the

enduring verities around the need for diversification – and

keeping flexible in the face of rapid change – came through. The

gyrations of government policy in the US, such as around tariffs,

for example, have tested investors’ nerves and galvanised

thinking about hedging strategies and ways to manage risk.

“The key over the coming quarters will be to remain selective,

diversify across asset classes and regions, and seek value in

areas where fundamentals are stronger than current pricing

suggests,” Nuveen’s Cooper said. “While headline risk remains

elevated, opportunities are emerging. We are incrementally more

positive on US large-cap equities due to robust earnings

resilience and improved sentiment. Fixed income markets offer

compelling yields, particularly across municipal bonds and

securitised assets, whilst real assets and listed infrastructure

also provide potential income and stability. Strategic allocation

needs to account for ongoing volatility but also avoid

overreaction to short-term noise.”

“In an environment characterised by policy unpredictability and

sharp swings in sentiment, we are seeing greater use of

derivative overlays, particularly options strategies to manage

downside risk and enhance income,” Cooper continued. “These are

often integrated into multi-asset portfolios and explained to

clients as tools to cushion volatility or monetise periods of

heightened uncertainty. Cost is carefully weighed against

potential benefits, with strategies typically stress-tested and

reviewed regularly. Transparency is key, and clients are

increasingly familiar with these instruments being part of a

robust risk management toolkit.”

Unduly unloved

Certain asset classes deserve more attention, argues Nuveen’s

Cooper.

“We believe municipal bonds have been unfairly discounted.

Despite solid state and local fundamentals, they have lagged

broader bond markets this year. With yields close to decade highs

and a steeper curve than US Treasuries, we see value particularly

for long-term investors. Real estate also appears overlooked.

While office remains challenged, sectors such as senior housing,

grocery-anchored retail and medical office space are supported by

structural demand drivers. Infrastructure, especially related to

energy and data, deserves renewed focus due to growing power

demand and supply constraints,” she said.

Quite contrary

In all the conversations about asset allocation, it is noticeable

that wealth managers are keen to differentiate their styles and

stand out. That can include taking a contrarian investment

philosophy.

“One contrarian stance we hold is a continued overweight to US

large cap equities, particularly given the `sell the US’

narrative that dominated earlier this year and ongoing concerns

of stretched valuations,” Cooper said. “Despite geopolitical

tensions and currency pressure, fundamentals remain strong, as

captured in second quarter earnings, with profit growth still

expected to outpace Europe and China in coming quarters. We are

also constructive on securitised credit and preferred securities,

where spreads and fundamentals offer attractive entry points,

even as other investors remain cautious. Lastly, we believe the

infrastructure demand, linked to AI and electrification, is

underestimated by the broader market.”

Jim Caron, chief investment officer of the portfolio solutions

group of

Morgan Stanley Investment Management, is also going against

the "sell the US" narrative.

"We think full-year 2025 earnings estimates may be understated in analyst expectations by about $9, based on the historical relationship implied by the run rate of the year’s earnings. This may be because analysts are hedging downside economic surprises due to the fallout from future tariffs. We think data slogs through, which provides room for upside earnings surprises in the second half of 2025. This would not only lead to further earnings increases into 2026 but also suggest that current P/E valuations may be overstated. It is the basis of why we are looking to add to US equity exposure for the second half of this year.

This publication asked Caron for some tactical as well as

strategic asset allocation views.

"The second half of 2025 will resolve the uncertainty stemming

from first half of the year surrounding tariffs, budget and tax

policies in the US. It remains to be seen if the fallout from

tariff policies leads to a more pronounced slowing of economic

activity and higher inflation - the stagflation scenario - or if

the economy muddles through without a recession. Our view is the

latter. The resolution of the US budget and tax plan could be a

tailwind for economic activity as it may add stimulus through

accelerated depreciation, increased capital expenditure (cap-ex)

and further deregulation that shifts the engine of growth from

the government to the more productive private sector.

“We expect more productive growth over the next sis months. An

underappreciated change in policy is the reduction in Federal

outlays/spending that is starting to take hold. Post Covid,

government spending and policies influenced and crowded out

private sector activity from employment growth to Green

initiatives that influenced corporate spending and investment.

This change in policy is hard to measure immediately but instead

shows up in business investment and [capital expenditure], which,

in turn, feeds into GDP. The big difference is that it is driven

by the private sector, not public, such that invested money has a

higher multiplier effect,” Caron said.

Asset allocation approaches are changing in a variety of sectors,

including among philanthropists.

Most charities expect to pivot more of their capital towards

active investments amid volatile markets and shift their

investment portfolios towards equities and alternatives over the

next two years, according to interviews with senior charity

executives conducted for Rathbones. The UK wealth manager talked

to 100 UK charity board directors, finance directors, investment

managers and investment directors with a collective £3.7 billion

of stock market related investments. The survey found that 87 per

cent expect their active investment allocations to increase,

either slightly (49 per cent) or dramatically (38 per cent) over

the next three years.