The following comments were made by Matthews Asia, the US-headquartered investment house that focuses – as its name suggests – on the Asia-Pacific region. The views here are republished with permission. The article’s author, Andy Rothman, discusses a significant concern about whether rising volatility will prove a particular headache or not for wealth management clients, and suggests how people should view it.

Rising volatility in China is a consequence of economic modernization and should not be feared by long-term investors.

While it is inevitable that China will, on average, grow a bit more slowly every year for the foreseeable future, rising volatility is a consequence of economic modernization and should not be feared by long-term investors.

Having bet its future on the success of private enterprise, Party leaders are just now growing comfortable with the idea that capitalism must allow for failure.

Only 10 per cent of new homebuyers are speculators, with 90 per cent of sales going to owner-occupiers. And Chinese homebuyers have a lot of skin in the game: they must put a minimum of 30 per cent down for a mortgage.

The media reports daily on the increasingly tumultuous state of the Chinese economy. One private firm goes bust. Another misses a bond coupon payment.

What great news! Bring on the failures!

Inevitable

While it is inevitable that China will, on average, grow a bit more slowly every year for the foreseeable future - consider the base effects and a shrinking workforce, among other factors - rising volatility does not signal impending doom. Instead, it is a consequence of important, and largely positive, structural and philosophical changes underway in China today.

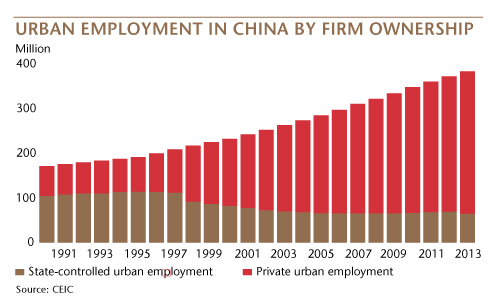

The most significant structural change is the growth of China’s private sector, which is now the driving force of an economy that had no entrepreneurs when I first worked there 30 years ago. That all began to change in the late-90s, when the Communist Party eliminated 46 million state-sector jobs over six years. That’s equal to sacking 30 per cent of today’s US labour force, but few outside of China remember that dramatic start to the reform process, or understand that those layoffs were accompanied by the largest one-time transfer of wealth ever seen, as state-owned housing was handed over, for a nominal fee, to Chinese workers.

Today, 83 per cent of the urban workforce is private and almost all new job creation is by private firms. Private companies account for about 70 per cent of investment and industrial sales, and the largest share of profits among larger industrial firms. The state still controls the financial sector and most capital-intensive companies, but China has become very entrepreneurial over a very short period of time.

As the economy becomes increasingly market-driven, greater volatility is inevitable. We know that market economies cannot avoid periodic recessions, and in the future, this will apply to China, especially if the Party continues to open up the financial sector.

This liberalisation should be welcomed by everyone who has urged the Party to expand economic and personal freedom for its citizens and its enterprises. Investors have learned to deal with volatility in developed markets, and they need to do so in China, acknowledging it as a sign of economic development.

The important philosophical change is the Communist Party’s recent acceptance of the concept of creative destruction. Having bet its future on the success of private enterprise, Party leaders are just now growing comfortable with the idea that capitalism must allow for failure. As with previous reforms, this change will be implemented gradually and cautiously.

We’ve seen the first stages of this, as local governments have apparently been instructed to refrain from bailing out a few small, distressed private companies.

Death watch

The media has been staging a “death watch” in the city of Ningbo, waiting for the failure of a single residential property developer. But, here too, failure should be embraced. There are probably 90,000 developers in China, although I’d be surprised if more than 1,000 have more than one project underway. Would it be that shocking to discover that a few of these firms are poorly managed, and would fail if the Party didn’t prop them up?

This reflects a healthy and confident evolution of policy and should be welcomed. This is the kind of change which should, over the long run, result in a more sustainable economy and a more open society; the kind of change that should lead to many more successful, privately-owned, listed companies.

Finally, a few more words about China’s residential property market, which must be viewed through the lens of the structural and philosophical changes discussed above. Begin by noting that the massive transfer of once state-owned apartments represented the initial liquidity for the ongoing sale of commercially-built flats that started only about 15 years ago.

Only 10 per cent of new homebuyers are speculators, according to surveys, with 90 per cent of sales going to owner-occupiers. And Chinese homebuyers have a lot of skin in the game. About 20 per cent of sales are all-cash, and owner-occupiers must put a minimum of 30 per cent down for a mortgage. When investors can get a mortgage, they must put at least 60 per cent cash down.

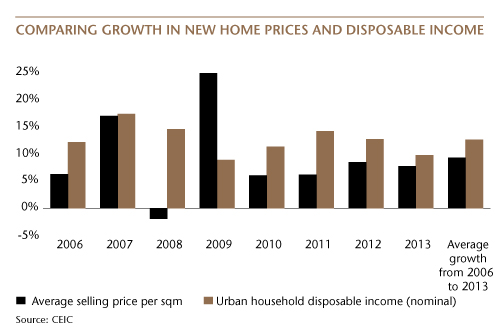

Real estate (residential, office and commercial) has an outsized role in the economy, including accounting for about a fifth of all bank loans, but mortgage-backed securities are almost non-existent, limiting significantly the contagion risk of falling prices. New home prices have risen sharply, by an average of 9 per cent annually over the past eight years, but nominal urban income has risen even faster, by 13 per cent per year.

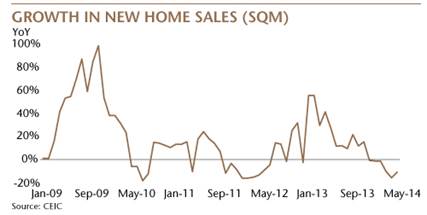

Finally, remember the base. A decline of 9 per cent year-over-year in new home sales (by volume) during the first five months of this year sounds far less scary if we know that sales rose by 38 per cent during the same period last year. Sales rose by only 2 per cent to 4 per cent YoY during 2011 and 2012, and the world didn’t end.