The following article is by Greg Harris, senior investment manager at , the South Africa-headquartered asset management firm.

Few money managers would be willing to describe today’s global equity markets as cheap or offering great long-term value (they certainly offer less than 18 months ago). Similarly, the voices supporting bonds as a long-term investment thesis have grown steadily quieter, especially as the US Fed stands in the corner ready to unleash further tapering.

Risk-taking investors are faced with a very basic conundrum – own equities because there is nothing else you would rather own (and the usual alternative to owning equities - i.e. bonds - is about as attractive as you with a kebab in your hand at 3am) or become more risk averse and hold cash.

The first possible solution to this conundrum is to entrust your money to people who are still able to find the diamonds in the rough, but remain exposed to the same asset classes. Short-term performance for such managers can often diverge significantly from market benchmarks and remaining invested requires patience and a strong belief that you were skilled or lucky enough to select the right manager.

A second possible solution is to find an alternative asset class that offers a more attractive risk and return profile due to its design rather than its current valuation. Enter convertible bonds.

Convertible bonds are a relatively elusive yet fundamentally attractive asset class. Very low issuance relative to traditional bonds has in the majority kept them the preserve of professional money managers.

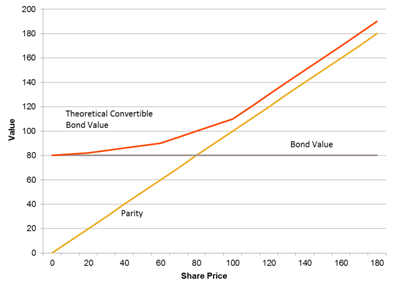

A convertible bond is most easily thought of as a traditional bond issued by company X, together with a call option on the stock of company X. The owner of the convertible bond in effect owns both a bond and a call option on the underlying equity, resulting in a payoff profile as shown in Chart 1.

Chart 1 – Convertible bond valuation as a function of equity price

Globally convertible bonds shot to prominence during the 2008/09 financial crisis for all the wrong reasons. Up until then they had been significantly invested into by convertible bond arbitrage hedge funds and proprietary trading desks, which estimates suggest accounted for 80 per cent of the market. The funds had levered positions and during the turmoil needed to reduce risk quickly.

The result was many sellers and few buyers, creating a liquidity crush and pushing prices down, a very bad story for levered investors. Even so, convertible bonds lost less than equities did during 2008 and recovered strongly in 2009 as markets recovered and liquidity normalised. The long-term risk-adjusted return numbers are attractive relative to equities.

Today it is suggested that the investor base has changed significantly, with a much larger institutional (and unlevered) investor base that is less likely to be forced to close out positions during a stress event.

The attraction of convertible bonds in a market such as we find ourselves in today is that they share the positive characteristics of both bonds and equities – if equities go up, they will participate (to a varying extent) in the rally, and yet if equities fall they should experience the capital preservation characteristics of a traditional bond.

Much like equities, it is probably fair to say that convertibles are priced reasonably and that this is not an allocation without risk. However the very nature of a convertible bond, with its asymmetric payoff profile, makes it an interesting instrument to be exposed to at a time when there is much market manipulation by central banks in asset markets.

Convertible bonds benefit during times of significant equity dispersion as their convexity (increasing participation as equities rise) means that you will often make much more on your winners than what you will lose on the losers if you purchase them close to the bond floor. Instrument selection is important, but not as critical as for those in traditional equities.

M&A activity

Convertible bonds have an added complexity due to their embedded derivative nature, and many include clauses which protect the owners in the event of a merger / acquisition of the company. These terms vary by bond but can be massively advantageous to the owners of the bonds. In a world of increasing M&A these take-out premiums offer a further value enhancement strategy for owners of the asset class, provided you know where to look.

What is in it for the issuers?

Convertible bonds are attractive to CFOs who are able to keep their cash borrowing costs down (i.e. the interest rate they pay on borrowed money) by offering investors a "free" call option on their stock. Inherently this must lead to some biases within the convertible bond universe and cash-flush corporates who can raise money at very low rates in nominal bond markets are unlikely to be found issuing convertible bonds.

Investing in this market is a specialised activity and it would be difficult for an investor to build a portfolio of names without spending significant time researching the asset class, and understanding the intricacies of each issue. There are however a number of global funds with a variable focus on the asset class and a handful that are managed by boutique convertible bond managers that have focused solely on the asset class for decades.

A couple of basic truths never change irrespective of the asset class, that is don’t overpay for the underlying assets and understand what you are buying.