Is the Renminbi on its way to internationalisation? says "yes, but not quite there yet."

China is now the third largest economy and the largest export nation in the world. Given its high potential growth, the position of China in the global economy will only increase over the coming years. However, the role of RMB whether in transaction or investment has been far less represented compared with where China is in terms of trade volume and economic size.

Arguably, this is largely the result of policy choice. Since China has opened up, the country has adopted a fairly cautious attitude towards currency liberalization and has instead focus on fixed asset investment and the export industry. However, there is a shift in attitude in the past few years as evidenced by a paper published in 2006 by the working group of the People’s Bank of China, embracing currency internationalisation and affirming the benefits to China.

What does it mean to internationalise a currency?

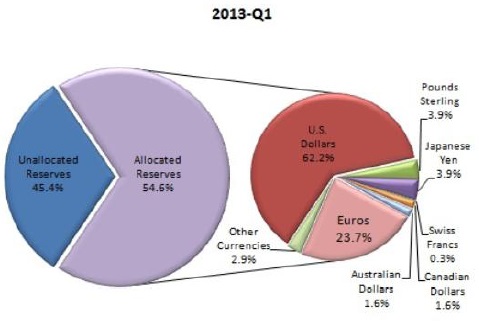

In the last few years, the use of the RMB as a transactional currency has been established and rising with China’s rising importance in global trade, its use as a financing and investment currency remains limited. According to the IMF, based on data as of 1Q13, the dollar and euro remain the most dominant currencies held by central banks around the world. China’s financial markets have also remained largely insular with significant barriers to global participation. According to the ADB, the total size of China’s domestic bond market is $3.9 trillion as of June 2013, and compared with the $59 billion of QFII and RQFII has been approved as of July 2013.

Currency Compisition of Official Foreign Exchange Reserves Source (IMF)

Why internationalise?

There are a number of benefits why China would like to pursue internationalisation of its currency.

Firstly, when more trade and financial transactions are settled and invoiced in RMB, it reduces the transaction and hedging costs for Chinese companies.

Secondly, an internationalised RMB would facilitate Chinese companies to invest abroad. China is already one of the largest foreign direct investors in the developing world. China has a high savings rate and it would be advantageous to recycle the surplus savings to the rest of the world.

Thirdly, having an international currency would enable China to borrow in its own currency. The international reserve currency status of the US dollar is one reason why the US is able to run a persistent current account deficit without triggering an external debt crisis.

Fourthly, the holding of RMB by non-residents would enable China to collect seigniorage (the margin between the denomination of the notes and the cost of issuing the notes obtained by the note issuer) from the rest of the world or at least reduce the amount that is being paid to the US. Finally, internationalisation of the RMB could help China to preserve the value of its foreign exchange reserves.

Currently, China is the largest holder of foreign exchange reserves in the world with an estimated asset value of over $3 trillion. It is estimated that more than 70 per cnet of the assets are denominated in dollars. This leaves China vulnerable to US monetary policy which might have a direct impact of the value of the dollar resulting in capital losses for China. An international RMB would suggest that the Chinese central bank is able to hold more of its foreign claims in its own currency.

Roadmap and Pathway to Internationalisation

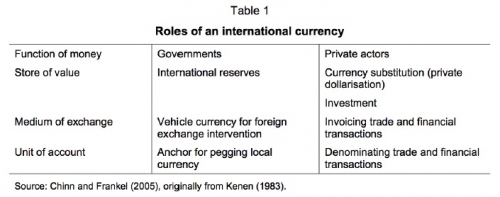

According to Chinn and Frankel (2006), the three most important international reserve currency determinants for an international currency are: economic size, depth of the financial market and the rate of return. The size factor is undoubtedly favorable for China but the development of its financial markets has some way to go.

One important contributing factor to the preeminence of the dollar as an international currency is its deep and developed financial markets. Accordingly, the collapse of the Bretton Woods system did not brought about the demise of the USD as an international currency. The other precondition would be the transition towards full currency convertibility. Currently, the RMB is convertible at the current account but not at the capital account. Without full convertibility, it would be difficult to expect residents and non-residents to accept the RMB for a broad variety of purposes.

Investment Implications

1. Deepening of the RMB investment universe

The internationalisation of a currency is likely to be a gradual process than a one-off event. In the case of China, the establishment of Hong Kong as an offshore RMB center and at the same time expanding access to the onshore market through QFII and RQFII schemes is evidence that China favors a dual track model. The amount of RMB deposits in HK stands at RMB698 billion as at May 2013.

As a result, the amount of CNH products has risen most especially in fixed income. However, compared with the RMB100 trillion of deposits in the onshore system, the offshore market has plenty of room to grow. Overtime, it is also crucial for a liquid offshore swap curve to anchor bond pricing as well as supporting the pricing of a wider range of derivative products. This is necessary to attract a broader variety of investors to participate in the market.

The current QFII system is likely to be expanded. Recently, China has announced that the QFII ceiling will be raised from $80 billion to $150 billion while the RQFII scheme will be extended to Taiwan, Singapore and London. This remains baby steps compared with the total market cap of 2.9 trillion in the China onshore equity markets and 3.9 trillion in the fixed income markets.

The current QFII system is likely to be expanded. Recently, China has announced that the QFII ceiling will be raised from $80 billion to 150 billion while the RQFII scheme will be extended to Taiwan, Singapore and London. This remains baby steps compared with the total market cap of 2.9 trillion in the China onshore equity markets and 3.9 trillion in the fixed income markets.

2. Macroeconomic and currency impact

The pathway to internationalisation is likely to be preceded by macroeconomic and currency stability as the currency needs to first gain confidence for non-residents to hold as a store of value. A strong and stable RMB in the midst of recent challenges in the developed world has brought the attention of international investors.

The process of internationalisation could result in an appreciation bias as pent up demand supports the value of the currency. This was the case of the Australian dollar as more international investments were drawn than borrowings after internationalisation. Some studies have also suggested that internationalisation has brought down long term interest rates for Australia.

Countries with a strategic export orientation had tended to perceive internationalisation with some degree of caution as currency volatility could adversely affect its competitiveness and economic growth. This was the case of Japan and Germany in their 1970s. To raise the tolerance of the economy to currency volatility, China would also need to reform its economy towards more consumption and higher value exports.

Over the long run with full convertibility and global trading, currency volatility will increase from the current low levels. An international currency is also more vulnerable to speculative attacks and the monetary authority would have less control on the currency.

3. Impact of Chinese liquidity on global asset prices.

China has been running persistent current account surpluses for many years. It has a huge savings rate with M2 more than 2 times its GDP. Much of the liquidity is “repressed” with deposit rate controls and limited investment opportunities available in the domestic market. The search for yields and better return is arguably a contributing factor behind high real estate prices and the proliferation of wealth management products.

Looking forward, the internationalisation roadmap goes beyond opening up China’s financial markets to the outside world, but also allowing Chinese savings to tap global investment opportunities.So far, the only avenue is through the QDII scheme which is relatively small. Undoubtedly, the scheme will be expanded both in scope and magnitude. In the long run when Chinese liquidity is allowed to freely participate in global markets, there will be implications for global asset prices. The net impact will depend on how much inwards investments China obtains as a result of opening up.

Conclusion

Even with strategic will, the internationalisation of the RMB is likely to be a long process. According to Frankel (2011), the US had surpassed the UK in output, trade and net creditor position by 1919 but only surpassed as the number one reserve currency with a lag by 1940-45. A number of prerequisites are not there yet: currency convertibility, deep financial markets and a resilient financial system. Ultimately, the decision to internationalise the RMB can only go as far as it is beneficial for China. For a country as large and important as China, the road there would create both risks and opportunities for an investor.