The following comment comes from and is republished here with permission.

The results of the 2020 election were made final on Wednesday, two months after Election Day. It all came down to the pair of runoff races in Georgia, where Democrats won control of the Senate. With former Vice President Joe Biden winning the White House, a 50-50 split in the Senate allows Vice President Kamala Harris the deciding vote in a tie, handing Democrats the majority in both chambers of Congress. The House and Senate also convened on Wednesday in a joint session to count electoral votes. We were saddened by the violent events at the US Capitol in what is a normally symbolic affair affirming the president-elect's victory.

Let’s take a look at what happened in Georgia, its impact on the new administration’s policy priorities and what it may mean for the markets and your portfolio.

What happened in Georgia

In two very competitive races, Georgia voters determined which party controls the Senate. In one contest, Democratic candidate Rev. Raphael Warnock defeated incumbent Republican Senator Kelly Loeffler. In the other, Democrat Jon Ossoff defeated incumbent Republican Senator David Perdue. This gives Democrats control of both chambers of Congress.

The runoff elections were a result of Georgia’s election in November, in which none of the Senate candidates received a majority of the vote. Under Georgia law, if no Senate candidate gets more than 50 per cent of the vote, the two candidates who receive the most votes, regardless of party, compete in a runoff election. Georgia had two separate Senate races this year, thanks to a special election to replace the retired Senator Johnny Isakson.

Expected policy focus for the Biden administration

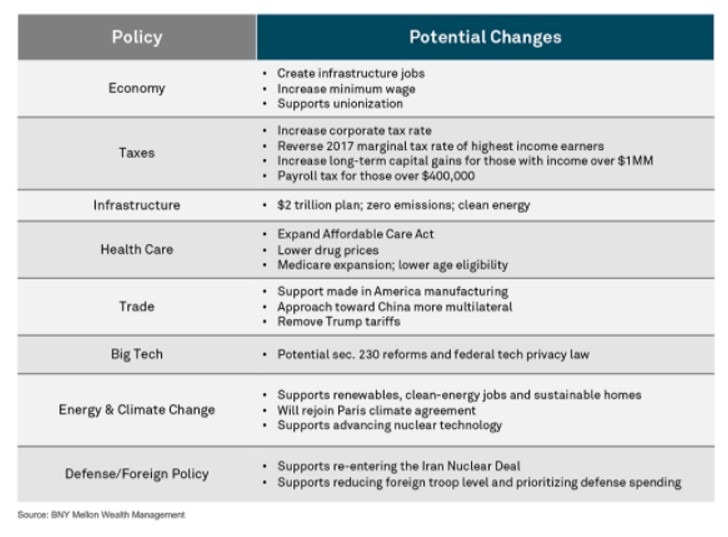

A slight majority in the Senate gives Biden more room to pursue his agenda of fiscal relief, infrastructure, green energy and higher taxes (as highlighted in Exhibit 1). Having said that, the political divide is very thin both in the Senate and the House of Representatives. Nevertheless, the George W. Bush and Obama administrations were able to pass major legislation with less than 60 votes in the Senate, including the Bush tax cuts, which were passed with a 50-50 Senate.

Exhibit 1: Biden's Policy Platform

In the early days of Biden’s administration, the focus will most likely be on addressing the pandemic and ensuring the US economy can continue to recover despite showing some recent signs of moderation. We expect that the emergency coronavirus relief package passed in December will be followed by more stimulus as early as February, with higher direct payments to individuals likely.

Other areas of spending, including infrastructure, heathcare and clean energy, can be enacted through the budget reconciliation tool. This process allows the Senate to pass legislation with just 51 votes and for funding to be paid for over 10 years. To pay for these initiatives, we will likely see some form of higher taxes, with a corporate tax increase having the most support; an increase in personal taxes may possibly be off the table until the recovery is under solid footing. Also, since trade policy is controlled by the executive branch, Biden's support of free trade should help allay fears of more protectionist policies, helping to support global growth.

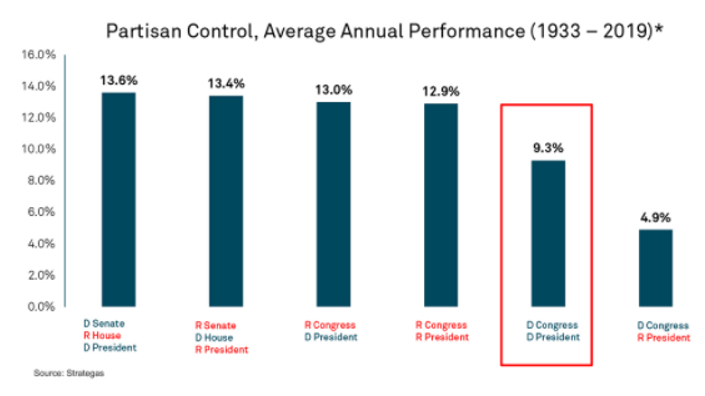

Although equity markets tend to like divided governments, as illustrated in Exhibit 2, a single party can still be positive for stocks. As history reminds us, a single party controlling the White House and Congress is often short-lived. Presidents Bill Clinton, George W. Bush and Barack Obama saw their parties control both houses of Congress when they were first elected and each lost that majority in the first mid-term election.

Exhibit 2: What History Tells Us

The impact on markets and portfolios

Equity markets and interest rates moved higher on Wednesday following the Georgia Senate outcome given the increased clarity on the makeup of Congress and growing expectations for more fiscal stimulus. The S&P 500 and Dow Jones Industrial Average were up 0.6 per cent and 1.4 per cent, respectively. Meanwhile, the Nasdaq Composite declined 0.6 per cent, as technology names lagged. Smaller capitalization stocks, as measured by the Russell 2000 index, jumped 4 per cent. The US Treasury yield curve also steepened, with the 10-year Treasury note yield above 1 per cent for the first time since last March.

Although at the time of the November election many market participants believed a so-called “blue wave,” where Biden won and Democrats took control of both chambers of Congress, would lead to an equity market selloff, at present investors are focusing on the near-term benefits of more fiscal stimulus and less on potential tax changes down the road. The markets are discounting brighter days ahead as vaccinations get rolled out, monetary and fiscal policy remains supportive and the path of the recovery gains momentum.

We have positioned portfolios for a more cyclical, global recovery (Exhibit 3). We expect stronger growth to be reflected in higher yields, a steeper yield curve, a rebound in earnings and a weaker dollar. As such, we continue to favor equities over bonds and look to further take advantage of the rotation from growth to cyclical stocks – a trend we’ve been acting on since last summer. At this week’s meeting of our Investment Strategy Committee, we continued to recommend taking profits from US large cap stocks and move to those asset classes which are tied more to the cyclical, global recovery, such as US small cap stocks and emerging market equity. With expectations for more fiscal stimulus and the potential for higher taxes down the road, municipal bonds should also provide attractive yields for tax-sensitive investors within a diversified fixed income portfolio.

Exhibit 3: Asset Class Positioning: Investment Strategy Committee Recommendations

It has certainly been a unique election cycle but it is important not to put too much weight on political outcomes and instead stay focused on your long-term wealth objectives. We believe our clients are well-positioned for this political and economic landscape and we will continually evaluate policy impacts on business, economic and capital market cycles.