The following commentary comes from Christian Armbruester, chief investment officer of the European firm , who regularly airs views in these pages. This publication recently attended a seminar held in the firm’s offices in Richmond-on-Thames, and was struck by Armbruester’s discussion of foreign currency volatility and how deciding whether to hedge forex risk or not can be a tough call. So we asked him to elaborate on his presentation here. We are very grateful to Blu Family Office for sharing these insights. As ever, of course, the usual editorial disclaimers apply. If readers want to react, they can email tom.burroughes@wealthbriefing.com and jackie.bennion@clearviewpublishing.com

The world is a big place with more than 200 countries and an almost equal amount of different local currencies. Any investor who is seeking global diversification in their asset allocation, would therefore have to exchange much of their money from one currency to many others. How much? That is a matter of strategy and also mechanics. After all, not everyone can simply exchange so many different currencies in a cost-effective manner. One thing is for certain: the minute we do anything we are at risk and there are also costs. Here is the journey we took as a family office, to figure out what would be the most optimal way of investing our money into the world.

The first thing we noticed is that we do not need to invest in every country. The top 50 countries make up 95 per cent of global gross domestic product and operate on 35 currencies. The marginal benefit of investing in Iraq or Zimbabwe seemed rather small versus the high cost and additional administrative burden. That made things simpler, but the more complicated question we had to answer was: how were we going to measure our success of investing? We needed a reference currency, or “base-currency”, as it is often called. Simply put, it is the currency that matters to you – where you live, where you draw income, where you pay your bills and what you are ultimately investing so that you can get more.

The next decision we had to make was, how much of our money were we going to convert. How much do we buy in the US or in Europe and what about Yen or Brazilian Real? There are wonderful investment opportunities everywhere and in so many different currencies, it really is difficult to say how much we would want of each part of the rest of the world. Some try to categorise the world by economic strength, others by the value of the local stock market, and even some look at growth. The fact is, no matter what you do, a large portion of your risk and returns from your investment activities will be determined by how much you retained in your base currency.

Let’s look at the numbers. Say 10 per cent of your money is in sterling and 90 per cent in all the other currencies, as part of your globally diversified investment strategy. And please note that sterling has even less than a 10 per cent weight in the MSCI World index. What happens if sterling goes down? Then you have made money in all the other currencies and when you convert those into the weaker pound, you have more than you had before. But what if sterling goes up? Then you would lose on 90 per cent of your portfolio. In other words, if there was such an event, such as no hard Brexit, and sterling were to re-trace some of the 20 per cent it lost against all the other currencies after the referendum, it could result in huge losses.

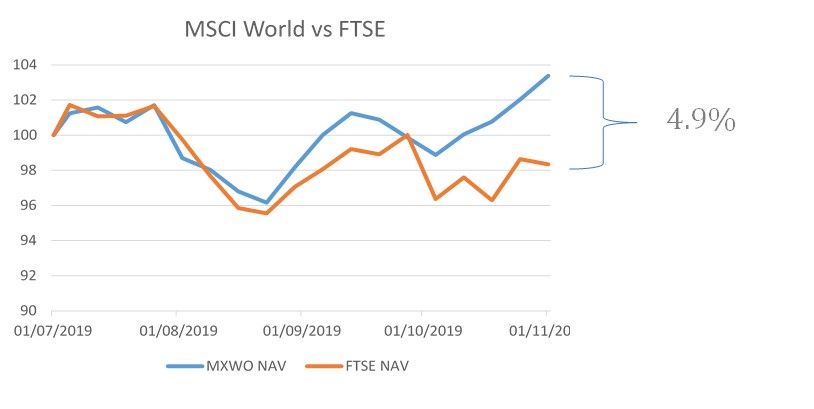

The chart below shows the performance of the FTSE 100 index versus the MSCI World index since July. Sterling has appreciated more than 6 per cent since then, which means those companies that export into other countries have lost a lot of their revenues relative to sterling which explains the almost 5 per cent underperformance.

Source: Blu Family Office

Can we hedge this risk and not worry about currencies at all? You could invest only in your base currency. But the whole idea of diversification is to invest in other things and how many people in Argentina had wished they had put their money abroad? It can always go horribly wrong and the only thing we know for sure, is not to put all your money into any one thing. You have to take risk in different regions, opportunities and denominations to manage wealth effectively.

The other way to manage currency exposure is through the financial derivatives markets. There, we can buy forwards, calls, puts and even futures on any currency we like, allowing us to hedge whatever risk we wish to take off. There is a price, of course, which is not only a function of the spreads and execution costs, but also the interest rates in the countries with different currencies. Say you wanted to hedge US dollars into euros, then your costs are currently more than 2.5 per cent, as interest rates in the US are still relatively high compared with negative rates for the euro. Not something you want to be paying for the next 25 years, which is also why it is not economical to hedge all of your currency risk. And moreover, your currency could also depreciate, in which case the hedge would also cost in performance.

Complicated stuff, and there is no right or wrong answer, and your base currency will either go up or down. Whatever level of currency risk you choose to take on, remember this: the sheer size of the position warrants some serious consideration. The biggest risk of all is often the most obvious and therefore also the easiest to ignore.